Versicherungsunterzeichner

Wohin möchten Sie als Nächstes gehen?

Oder erkunden Sie diesen Beruf ausführlicher...

Was zeigt diese Schneeflocke?

Was ist das?

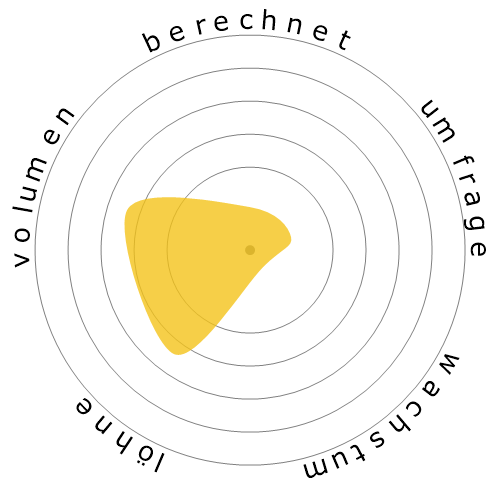

Wir bewerten Jobs anhand von vier Faktoren. Diese sind:

- Chance der Automatisierung

- Jobwachstum

- Löhne

- Anzahl der verfügbaren Stellen

Dies sind einige wichtige Punkte, über die man beim Jobsuchen nachdenken sollte.

Personen haben sich auch angesehen

Berechnetes Automatisierungsrisiko

Unmittelbares Risiko (81-100%): Berufe auf dieser Ebene haben eine extrem hohe Wahrscheinlichkeit, in naher Zukunft automatisiert zu werden. Diese Jobs bestehen hauptsächlich aus repetitiven, vorhersehbaren Aufgaben, bei denen nur wenig Bedarf an menschlichem Urteilsvermögen besteht.

Weitere Informationen darüber, was dieser Wert ist und wie er berechnet wird, sind verfügbar hier.

Benutzerumfrage

Unsere Besucher haben abgestimmt, dass es wahrscheinlich ist, dass dieser Beruf automatisiert wird. Diese Einschätzung wird weiterhin durch das berechnete Automatisierungsrisiko unterstützt, welches eine 83% Chance der Automatisierung schätzt.

Was denken Sie, ist das Risiko der Automatisierung?

Wie hoch ist die Wahrscheinlichkeit, dass Versicherungsunterzeichner in den nächsten 20 Jahren durch Roboter oder künstliche Intelligenz ersetzt wird?

Gefühl

Das folgende Diagramm wird angezeigt, wenn genügend Stimmen vorhanden sind, um aussagekräftige Daten zu erzeugen. Es zeigt die Ergebnisse von Nutzerumfragen im Laufe der Zeit und bietet einen klaren Hinweis auf Stimmungstrends.

Gefühlslage über die Zeit (jährlich)

Wachstum

Die Anzahl der 'Insurance Underwriters' Stellenangebote wird voraussichtlich um 4,0% bis 2033 sinken.

Gesamtbeschäftigung und geschätzte Stellenangebote

Aktualisierte Prognosen sind fällig 09-2025.

Löhne

Im Jahr 2023 betrug das mittlere Jahresgehalt für 'Insurance Underwriters' 77.860 $, oder 37 $ pro Stunde.

'Insurance Underwriters' wurden 62,0% höher bezahlt als der nationale Medianlohn, der bei 48.060 $ lag.

Löhne über die Zeit

Volumen

Ab dem 2023 waren 101.310 Personen als 'Insurance Underwriters' in den Vereinigten Staaten beschäftigt.

Dies entspricht etwa 0,07% der erwerbstätigen Bevölkerung im ganzen Land.

Anders ausgedrückt, ist etwa 1 von 1 Tausend Personen als 'Insurance Underwriters' beschäftigt.

Stellenbeschreibung

Überprüfen Sie einzelne Versicherungsanträge, um das Ausmaß des involvierten Risikos zu bewerten und die Annahme der Anträge zu bestimmen.

SOC Code: 13-2053.00

Kommentare (8)

I am considering entering insurance underwriting because claims were very bad, I must say.

Would you say that computer automation is taking over all areas of underwriting (commercial underwriting, property & casualty underwriting, etc.)? I do hear that it is taking personal insurance by storm.

Also, I am REALLY trying hard to find similar jobs to underwriting/insurance in case underwriting doesn't work out.

I'm looking at cost estimating (outside of construction), property assessment, and budget analysis. According to the Bureau of Labor Statistics, you don't necessarily need a business or finance degree to go into these fields (I took several traditional/core business classes in school, and I also majored in a field much like "business psychology" - organizational development, which was in the business school).

Do you have any alternatives that you plan to explore in case you have to leave underwriting? Do you think any of the ones that I mentioned are feasible alternatives?

Thank you,

Carl Daniel

Do you mean to say that this definition removes the need for an underwriter? - "Review individual applications for insurance to evaluate the degree of risk involved and determine the acceptance of applications."

Oh, sorry, I just realized that you mentioned that this definition only applies to line underwriting, and that automation will decrease the need for line underwriters.

Thank you for clarifying that there are two types of underwriting - I wasn't aware of that. Underwriting is the only field in insurance that interests me, but I'm not into sales. I've been working in claims (and subrogation) for years, but it's not my cup of tea.

Since I don't have the educational background to be an actuary, underwriting is pretty much the only option left for me.

I've never heard of staff underwriting before - unfortunately, working in claims didn't teach me much about underwriting.

It seems like staff underwriting is the future of employment in underwriting.

You mentioned that commercial insurance/underwriting is hard to predict due to the constantly evolving and complex nature of insurance.

I'm considering getting my Associates in Commercial Underwriting while I search for a job in underwriting.

What do you think about the future of employment in commercial underwriting? Do you think there's any hope for cautious optimism, especially for staff underwriters in commercial underwriting?

Thank you,

Carl Daniel

Auf Kommentar antworten